Late submission

The new penalties for late submission will be on a points-based system; for each late return, the business will receive 1 penalty point. Once the penalty point threshold is reached, HMRC will issue a £200 penalty, and a further £200 penalty for each subsequent late submission whilst the business is in the threshold. Penalty point thresholds are different depending on whether you are ordinarily file returns monthly/quarterly/annually – these are 5/4/2, respectively.

If the business takes over a VAT-registered business as a going concern, any penalty points built up by the business will not be transferred.

If the business is part of a VAT group and the representative member is transferred, then the points are transferred to the new member they also do not get removed if the member leaves the group, it stays, unfortunately.

Penalty points stay with the business for 24/25 months, provided it has not reached the threshold in that time. If it has reached the threshold, then it will need to complete a period of compliance with HMRC. The period would be determined by HMRC, meaning that the business must have no late submissions or late payments.

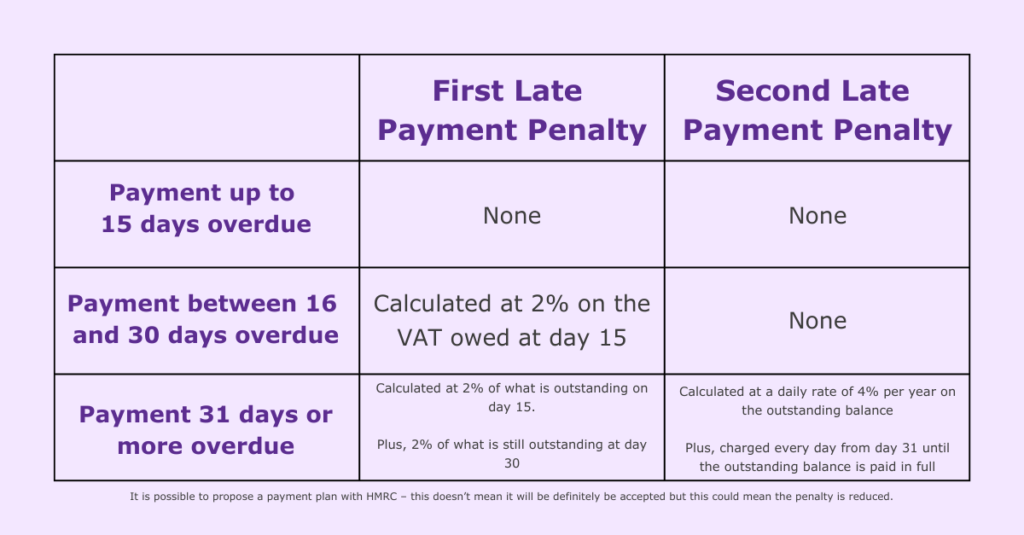

Late payments

There will be penalties for late payment and interest; these are dealt with separately. The earlier the business pays, the less the penalty will be. The table below shows the penalties that will be incurred for late payment.

Late Payment Interest

Interest will be calculated from the first day that the payment is overdue until the day it is paid in full. This is calculated at the Bank of England base rate + 2.5%.

Repayment Interest

The only good thing to come from this is HMRC will be making interest on repayments. The repayment interest is calculated at the Bank of England base rate minus 1%, with a minimum rate of 0.5%. Repayment interest is calculated from the day after the latter of these two dates:

- When the VAT was paid to HMRC (this is in the case where the client submitted the VAT return for a previous period, but actually, the return was for too much, and they need to make an amendment)

- The deadline for filing the return (repayment interest on VAT refund returns will be calculated from the filing deadline until HMRC make the payment)